From “eye watering” to “eye popping”

Much concern has been expressed about the longer-term consequences of the blowout in budget deficits and public debt in response to the economic hit from coronavirus. This is understandable given their scale. In Australia, the Treasurer described the projected budget deficit for this financial year of $185bn as “eye watering”. That’s more than three times the previous record of $54.5bn seen at the time of the GFC and at 9.7% of GDP is the highest since the end of World War 2.

And that was back in July! When the latest update is unveiled in the Budget next month it’s likely to be an “eye-popping” $230bn or so on our estimates, reflecting additional stimulus (including the bring forward of tax cuts, investment incentives, more infrastructure spending and stimulus payments) and the further blow to tax revenue from Victoria’s second wave. And given the ongoing hit to tax revenue and need for more stimulus it’s likely to remain big for several years, even though some of the stimulus payment programs will end once the hit to the economy recedes (we are assuming a vaccine and/or antivirals are successfully deployed next year to control the virus). Our revised budget projections are shown below.

Source: Australian Treasury, AMP Capital

This is likely to see the Federal Government’s gross public debt rise from around 34% of GDP (or $684.3bn) in June to around 54% of GDP (or $1.1trn) in three years’ time.

Our view remains that the Government has done the right thing. Fiscal stimulus has been necessary to protect businesses, jobs and incomes from the impact of the shutdown and associated uncertainty and without it we would be seeing a much bigger hit to the economy and ultimately to the budget and a slower recovery. And further near-term stimulus will be necessary to boost demand. But what about the longer-term consequences? Will the debt ever be paid down? Will fiscal austerity crimp the economy? Or do we live with higher public debt indefinitely?

The post WW2 experience

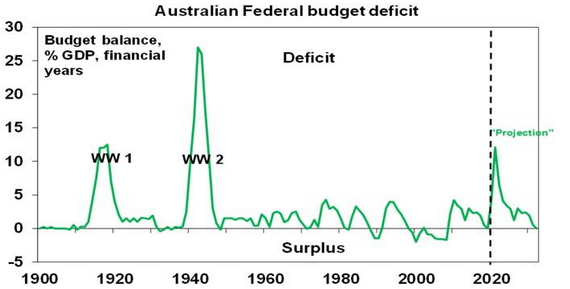

The current situation is not new. A similar challenge was faced after WW2. During WW2 the Federal Government’s budget deficit increased to a record 27% of GDP as a result of war time expenses. This was more than double the likely peak in the budget deficit this year of around 12% of GDP. See next chart.

Source: RBA, Australian Treasury, AMP Capital

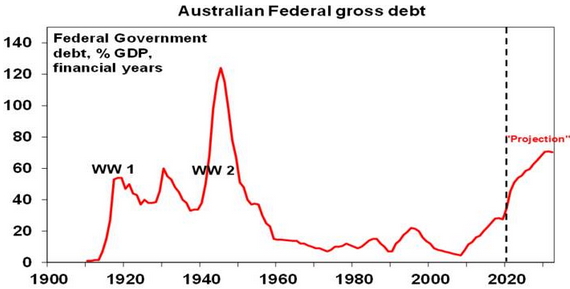

The huge war time budget deficits saw Federal gross public debt peak at 124% of GDP, which again is likely to far exceed the level it will reach in the years ahead. See next chart.

Source: RBA, Australian Treasury, AMP Capital

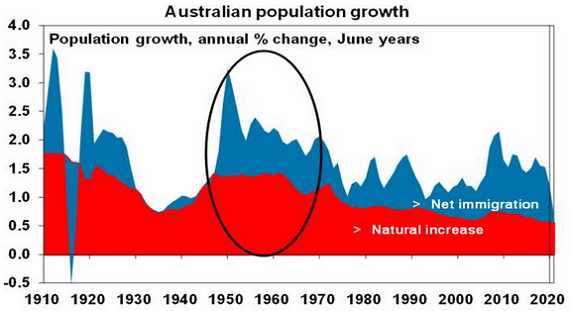

Interestingly the 1950s and 60s rarely saw balanced budgets let alone surpluses and so debt was not actually paid off. But the ratio of public debt to GDP fell sharply and by the early 1970s had fallen to 7% of GDP. The decline was facilitated by:

-

Low interest rates – between 1946 and 1970 10-year bond yields averaged just 4.5% pa; and

-

Strong nominal economic growth – between 1946 and 1970 nominal GDP growth averaged 10.1% pa.

See the circled area in the next chart.

Source: RBA, ABS, AMP Capital

The low interest rates (helped by prudential regulations that forced financial institutions to hold a certain amount of their assets in government bonds) contained the interest burden on the debt and the strong level of nominal growth meant that the debt burden declined relative to the size of the economy.

The strong growth in the nominal economy reflected:

-

Strong real GDP growth – which averaged 4.4% over 1946 to 1970. This in turn reflected a huge increase in the population from the post war baby and immigration booms. Between 1946 & 1970 population growth averaged 2.2%pa. See the circled area in the next chart.

Source: ABS, AMP Capital

-

And protectionist policies were employed to expand Australia’s manufacturing base which in turn helped employ the expanding population and boost productivity.

-

Inflation averaging 5.6% pa over 1946 to 1970 – mainly due to the Korean War boom.

So Australia grew & inflated its way out of its WW2 debt burden.

Can Australia do it again?

The Federal Government has so far ruled out big spending cuts (beyond the eventual ending of pandemic emergency programs) and another deficit levy. And for good reason – if people start anticipating a hike in taxes or cuts to public services they will behave accordingly, and this will endanger the recovery. Rather the Government has emphasised a strategy to boost growth – with the focus likely to be on tax reform, industrial relations reform, education and training, deregulation and increased infrastructure spending. More on this is likely to be announced in the October Budget. However, while these things will help and should be done, it’s doubtful they will get us anywhere near the post war real GDP growth rate of 4.4% pa:

-

Removing niggly taxes like stamp duty will help but to get a big productivity boost from tax reform would require a big shift away from personal and company tax towards the less distortionary GST – and that’s unlikely to get up politically.

-

Much of the low hanging fruit from industrial relations reform and deregulation has likely already been picked.

-

More infrastructure spending will help but it’s hard to see it accelerating much from the boom of recent years.

-

There is no baby boom in prospect and high unemployment will make a quick return to high immigration levels unlikely, so population growth (which this year will be its slowest since 1917) is likely to stay well below pre-covid levels of 1.6% pa, let alone the 2.2% pa seen in the post war era.

-

Finally, while some production of medical essentials may be brought back onshore, a return to full scale protectionism looks unlikely and would be counterproductive anyway.

Higher inflation would help but the RBA has been struggling to achieve that for a while now and high levels of unemployment mean that it is likely still several years away at least.

So, a re-run of the post war experience, which saw the debt burden decline rapidly as growth took off, looks unlikely. The budget and public debt projections in the first two charts above assume the same profile for budget repair from 2023-24 as occurred over the 2010-11 to 2018-19 period, and suggests that budget balance is unlikely until around 2032 by which time Federal public debt may have risen to 70% of GDP or over $2 trillion. Hopefully it doesn’t take that long, but the key point is that based on last decade’s experience we likely have to get used to a long period of high public debt to GDP levels. This is not necessarily a big problem.

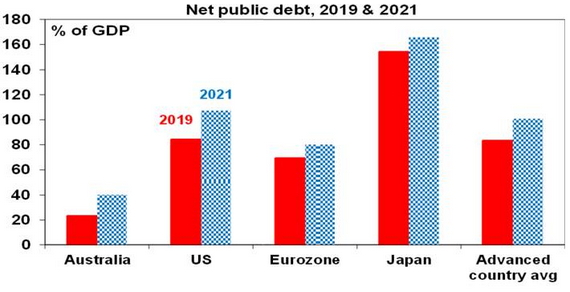

First, Japan, Europe and the US have been running high levels of public debt for years now without a major problem. In Japan gross public debt is already in excess of 200% of GDP, in the US its around 130% and Europe its nearly 100%.

Second, Australia’s starting point for net public debt last year was low at 23% of GDP compared with other advanced countries averaging 83%. And even with the projected blow out over the next few years it will still be relatively small. So, it’s not likely to be a drag on Australian assets versus other countries.

Source: IMF, AMP Capital

Third, one positive versus the post war period is that interest rates are even lower with the Government able to borrow for 10 years at 0.86% and for 3 years at 0.25%. This is well below what nominal economic growth is likely to be and so once budget deficits are reduced could help result in a faster decline in the public debt to GDP ratio than shown in the chart earlier.

Fourth, with Australia borrowing in Australian dollars and not dependent on foreign creditors, Australia is not at risk of a “foreign currency crisis” as a fall in the value of the $A will have no bearing on the Government servicing its debt.

Finally, it’s conceivable that if a problem arose the Government could cancel the bonds the RBA has purchased. This would mean a loss on the value of the government’s investment in the RBA, but it would be offset by a fall in its liabilities. Hence no big impact. The main constraint on this debt monetisation would be if inflation were to take off but that’s still a long way off.

Concluding comment

The bottom line is that the blow out in public debt is a concern and we may have to get used to a long period of relatively high public debt in Australia and in other developed countries. But this won’t necessarily cause a major problem.

Source: AMP Capital 22 September 2020

Important notes: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) (AMP Capital) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent of AMP Capital.